Accounting Treatment for an Asset Fully Depreciated and Continues in Used

What are Fully Depreciated Assets?

Fully depreciated assets mean that the assets can no longer be depreciated for accounting or tax purposes, and the asset's value is of the salvage value. It implies that the real depreciation has been provided in the accumulated depreciation account, and even though they have been completely depreciated either by SLM or WDM Method, taking into account the useful life of the asset, they continue to be a part of the balance sheet unless they are sold or destroyed.

- An asset can become fully depreciated due to two reasons:

- The useful life of the asset has been expired.

- The asset has been hit by an impairment charge, which is equal to the asset's original cost.

- In the balance sheet, if the accumulated depreciation on the liability side equals the asset's original cost, it means the asset has been depreciated fully, and no further depreciation can be provided and charged to the profit & loss account as an expense.

Table of contents

- What are Fully Depreciated Assets?

- Accounting for Fully Depreciated Assets

- 1) If the Asset has been Fully Depreciated

- 2) If the Asset has been Sold

- Examples of Fully Depreciated Assets

- Example #1

- Example #2

- Conclusion

- Recommended Articles

- Accounting for Fully Depreciated Assets

Accounting for Fully Depreciated Assets

The statutory accounting bodies have laid down guidelines and accounting standards to be followed for an accounting of depreciation and fully depreciated assets. Globally as per the recent implementation of the IFRS, it will be mandatory for all the companies to prepare their financials as per the IFRS rules and regulations.

- IAS 16 and IAS 36 are the accounting standards to be followed regarding the property, plant & machinery & impairment of the assets Impaired Assets are assets on the balance sheet whose carrying value on the books exceeds the market value (recoverable amount), and the loss is recognized on the company's income statement. Asset Impairment is commonly found in Balance Sheet items such as goodwill, long-term assets, inventory, and accounts receivable. read more .

- The company also has to disclose the same in the notes to accounts regarding the treatment given to a fully depreciated asset.

1) If the Asset has been Fully Depreciated

Since assets are the major components of the business, the full depreciation charged on them may have a significant impact on the financial statements of the company Financial statements are written reports prepared by a company's management to present the company's financial affairs over a given period (quarter, six monthly or yearly). These statements, which include the Balance Sheet, Income Statement, Cash Flows, and Shareholders Equity Statement, must be prepared in accordance with prescribed and standardized accounting standards to ensure uniformity in reporting at all levels. read more .

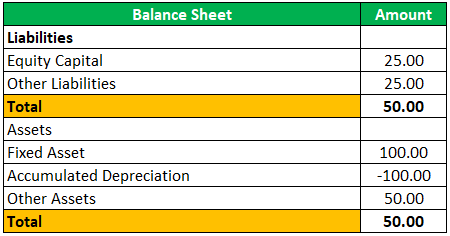

- A fully depreciated asset continues to form the part of the balance sheet, and the accumulated depreciation is reported on the liability side of the balance sheet.

- It impacts the income statement The income statement is one of the company's financial reports that summarizes all of the company's revenues and expenses over time in order to determine the company's profit or loss and measure its business activity over time based on user requirements. read more since a major portion of depreciation on the fully depreciated assets will not be recorded as an expense increasing the profits.

- Below is the presentation in the balance sheet:

2) If the Asset has been Sold

Suppose the fully depreciated asset has been sold. In that case, the total accumulated depreciation will be written off Write off is the reduction in the value of the assets that were present in the books of accounts of the company on a particular period of time and are recorded as the accounting expense against the payment not received or the losses on the assets. read more against the asset, and no impact will be given in the p&l statement since the total depreciation has already been recorded. The gain arising on the sale will be credited to p&l a/c has gained on the sale of assets.

Examples of Fully Depreciated Assets

Example #1

ABC limited buys machinery worth $ 2,00,000 on 01.01.2019 and depreciates the same on a slim basis for ten years, assuming there will not be any salvage value Salvage value or scrap value is the estimated value of an asset after its useful life is over. For example, if a company's machinery has a 5-year life and is only valued $5000 at the end of that time, the salvage value is $5000. read more of the term.

Solution:

IIn this case, ABC limited will record $20,000 per year as depreciation expense and credit the same to accumulated depreciation a/c. Below mentioned are the depreciation journal Entries Depreciation Journal Entry is the journal entry passed to record the reduction in the value of the fixed assets due to normal wear and tear, normal usage or technological changes, etc. where depreciation account will be debited and the respective fixed asset account will be credited. The main objective of a journal entry for depreciation expense is to abide by the matching principle. read more ABC limited needs to pass in their books along with the necessary disclosure and presentation in the balance sheet.

- Journal entry every year for the next 10 years:

- Journal entry at the end of term:

Example #2

Let's assume that a company purchased a building for $10,00,000. The company then depreciated the building Depreciation of building refers to reducing the recorded cost of a building until the value of the structure either becomes zero or reaches its salvage value. In addition, it helps to map the revenue in the form of lease rental generated during the corresponding expenses. read more at $200,000 per year for five years. The current market value of the building is $ 50,00,000.

Solution:

The company will have to record $2,00,000 as a depreciation expense by debiting the p&l a/c and crediting the accumulated depreciation a/c for five years. At the end of the 5th year, the company's current balance sheet will report the building at its cost of $1000,000 minus its accumulated depreciation of $10,00,000 (book value of $0) even if its current market value is $50,00,000.

- Such accounting is because the company continues to use the building for its business operations Business operations refer to all those activities that the employees undertake within an organizational setup daily to produce goods and services for accomplishing the company's goals like profit generation. read more and would continue to generate benefits for the company in the long term. Unless the company capitalizes on any further cost, which will improve the structure, no further depreciation would be allowed to be charged to the asset and reported only at each balance sheet reporting date.

- If the company plans to sell out the building at the current market value, the total accumulated depreciation would be written off against the building & the gain on the sale of assets will be credited to profit & loss a/c as "gain on sale of assets" thus inflating the current years profit by the gain amount.

- The building will not be reflected in the balance sheet since the same has been sold to a 3rd party.

Conclusion

Thus there are rules and procedures laid down by the accounting bodies of every country to follow the accounting treatment for the fully depreciable assets so that all the companies are comparable to each other. The auditor of the company is required to give an opinion on the truth & fairness of the company, along with whether the company follows all the accounting policies Accounting policies refer to the framework or procedure followed by the management for bookkeeping and preparation of the financial statements. It involves accounting methods and practices determined at the corporate level. read more laid down by the statutory bodies.

Recommended Articles

This has been a guide to Fully Depreciated Assets and its Definition. Here we discuss the accounting for fully depreciated assets and journal entries, along with Examples. You can learn more about accounting from the following articles –

- MACRS Depreciation

- Depreciation Rate Calculation

- Depreciation Tax Shield Calculation

- Accelerated Depreciation Calculation

Source: https://www.wallstreetmojo.com/fully-depreciated-assets/

0 Response to "Accounting Treatment for an Asset Fully Depreciated and Continues in Used"

Post a Comment